Top Transformational Leadership Coach to Follow – 2026

US-China AI Accord 2026: What the Tech Truce Means for Global Business | TheGlobalTitans

Introduction: The Handshake That Changed the Tech World In a move that stunned markets and policymakers alike, February 2026 witnessed the signing of the “US-China Framework for Managed Artificial Intelligence Competition” in Geneva. This accord, emerging after 18 months of secret backchannel negotiations, represents the most significant bilateral tech agreement since the Cold War. It doesn’t end the technological rivalry but establishes its first formal rules—creating what analysts are calling “competitive coexistence.” For global business leaders monitored by TheGlobalTitans, this isn’t just geopolitical news; it’s a fundamental recalibration of the playing field. The accord immediately removed a monumental “unknown unknown” from strategic planning, impacting everything from semiconductor investment decisions to startup funding routes and public market valuations. This analysis breaks down the agreement’s pillars and explores what this new era of structured tech competition means for innovation, markets, and the next generation of industry titans. The Accord’s Three Core Pillars: Decoding the Fine Print The framework rests on three mutually agreed-upon pillars designed to prevent catastrophic escalation while preserving national security: 1. The “Transparent Frontier” Pact on Foundational Models What It Is: Both nations have agreed to mandatory pre-deployment notification for the training of any AI model exceeding 10^26 FLOPs (a threshold marking the current cutting edge). This includes sharing basic safety testing protocols, not model weights or architecture. The Business Impact: This creates unprecedented predictability for hyperscalers like Google, Microsoft, and Alibaba. R&D roadmaps can now be planned without fear of a destabilizing, surprise “Sputnik moment” from the other side. For investors, it reduces the regulatory black swan risk that has plagued AI stock valuations. 2. The Semiconductor Supply Chain “Stability Corridor” What It Is: A tiered system allowing continued US export of mature-node (28nm and above) semiconductor manufacturing equipment to China, with enhanced tracking to prevent military diversion. In return, China agrees to discontinue direct state subsidies for legacy chip production that created global oversupply. The Business Impact: This brings strategic clarity to a $600 billion industry. US equipment makers like Applied Materials and Lam Research regain a stable, massive market for mature tech. Global automakers and industrial firms can expect an end to the volatile chip shortages and gluts of recent years. Taiwanese and Korean foundries (TSMC, Samsung) see reduced pressure in legacy nodes, allowing them to focus capital on advanced (<2nm) research. 3. The Joint Global AI Safety Initiative (GAISI) What It Is: A commitment to co-develop, with allied nations, international standards for AI risk in civilian domains: medical diagnostics, autonomous transport, and digital twins for critical infrastructure. Think of it as a “Paris Agreement for AI.” The Business Impact: For startups and tech titans alike, this promises a future of harmonized regulation. A company developing an AI radiology tool can now aim for a single global safety certification, not 50 different national standards. This drastically reduces compliance costs and accelerates time-to-market for ethical AI innovations. Immediate Market Reactions: Winners, Losers, and the Repricing of Risk The markets responded with a sectoral earthquake, repricing assets based on newfound clarity. The Clear Winners: Global Cloud & AI Infrastructure Stocks: Companies like Microsoft (Azure), Amazon (AWS), and Google Cloud saw immediate 5-8% jumps. Their massive capital expenditures in AI data centers are now backed by a more predictable competitive horizon. Specialized Semiconductor Equipment Firms: ASML (Dutch) and the US’s KLA Corporation rallied as the agreement protects their intellectual property while securing their China market access for mature technology. Multinational Manufacturers: Industrial giants with complex global supply chains, from Toyota to Siemens, welcomed the stability. Their stock gains reflected reduced fears of a tech Cold War fracturing production networks. The Sector Under Pressure: Pure-Play China Tech ETFs: Funds like KWEB experienced volatility. While reduced decoupling risk is positive, the removal of blanket state subsidies for some tech sectors forces a shift to genuine market competition. Cybersecurity “Cold War” Plays: Firms that had ridden the narrative of escalating US-China cyber conflict saw some momentum shift, as the accord includes basic protocols against AI-enabled offensive cyber operations. Certain Defense Contractors: While military AI development continues unabated, the shares of contractors solely focused on US-China tech warfare scenarios saw a slight pullback. The Strategic Recalibration: How Global Titans Are Adjusting In boardrooms worldwide, strategies formulated over the past five years are being rewritten. Key adjustments include: 1. The “Dual-Hub” Supply Chain Becomes StandardThe pre-accord model of aggressive “friend-shoring” (moving all production from China to allied nations) is evolving. Companies are now adopting a “China+1 for Mature Tech, Protected Hub for Advanced Tech” model. Example: A US electric vehicle maker will source its standard automotive chips and assemble battery packs in its Chinese joint venture (taking advantage of scale and efficiency), while manufacturing its proprietary AI self-driving computer solely in the US or a treaty ally. 2. Venture Capital’s New MapVC firms are recalibrating their investment theses: US/Europe Funds: Are now more willing to invest in hardware and semiconductor startups, knowing there’s a protected path to market without immediate, subsidized Chinese competition in their niche. Asian Funds: Are redirecting capital from “national champion” plays toward true frontier innovation in areas like biomimetic AI or quantum-classical hybrid computing, where the race is completely open. 3. The Rise of the “Globally Compliant AI” StartupThe joint safety initiative creates a massive new market niche. Startups that can build auditing tools, compliance software, and bias-detection frameworks that meet the emerging GAISI standards are attracting immediate investor attention. This is the unsexy, critical plumbing of the next AI decade. Long-Term Implications: The New Competitive Landscape Looking beyond quarterly earnings, the accord structures a new form of great-power competition. The Innovation Race Intensifies, But Shifts Arena: With certain boundaries set, the competition moves from raw, unfettered model scaling to breakthroughs in AI efficiency, novel algorithms (beyond transformers), and specialized hardware. It’s a race of quality over pure computational quantity. The “Third Pole” Gains Leverage: The EU, with its first-mover advantage via the AI Act, and nations like India, South Korea, and Singapore now have increased negotiating power. They can demand that US and Chinese firms comply with their standards to access their markets, shaping global norms from the middle. A New Class of Diplomatic-Tech Roles Emerges: Corporations are now creating Chief Geopolitical Strategy Officer roles.

2026 Crypto Market Analysis: Beyond Bitcoin & Ethereum’s Consolidation | TheGlobalTitans

Introduction: The Quiet Transformation of 2026 If you expected 2026 to begin with roaring crypto bull markets or catastrophic collapses, the reality is more nuanced—and arguably more significant. Instead of dramatic price surges, the first quarter of 2026 is characterized by a strategic consolidation. Bitcoin (BTC) has found a surprisingly stable range between $52,000 and $58,000, while Ethereum (ETH) experiences heightened volatility as it navigates its post-upgrade ecosystem. This isn’t market stagnation; it’s a foundation-laying phase. The “number go up” mentality of previous cycles is being replaced by a focus on utility, integration, and regulatory clarity. For the visionary leaders and investors in TheGlobalTitans community, this period represents a critical filtering mechanism. The speculative froth of the past has evaporated, revealing which projects are building durable infrastructure for the next decade of digital finance. The real story of early 2026 isn’t on the price charts—it’s in the quiet migration of value from purely digital speculation to tokenized real-world assets (RWA) and the meticulous rebuilding of institutional frameworks. The Current Landscape: Stability, Not Stagnation Bitcoin: The Institutional BedrockAfter the turbulence of 2024-2025, Bitcoin has emerged as a macro asset in consolidation. Its current price stability is underpinned by two opposing forces finding equilibrium: Persistent Institutional Accumulation: The spot Bitcoin ETFs approved in early 2024 (like those from BlackRock and Fidelity) continue to see steady, if unspectacular, net inflows from pension funds and long-only asset managers. These buyers view sub-$60,000 BTC as a strategic entry for portfolio diversification. Retail Apathy and Miner Pressure: Retail enthusiasm remains muted compared to previous cycles. Simultaneously, some miners, facing post-halving economics, are periodic sellers to cover operational costs, creating a consistent, predictable supply overhang. This creates a high-liquidity, low-volatility range that frustrates short-term traders but provides a stable base layer for the broader digital asset ecosystem. Ethereum: Volatility Through EvolutionEthereum’s path is more complex. Its price action is more volatile as the market digests the long-term implications of the “Scalability Completion” upgrades from 2024-2025. While transaction throughput is high and costs are low, the narrative has shifted. The “Ultrasound Money” Narrative Fades: With issuance now effectively net-zero or negative in many periods, the focus is no longer on ETH as a deflationary asset alone. The New Question: What is the primary driver of value? Is it as a consumable gas for decentralized apps (dApps), a stakeable security asset, or the settlement layer for trillion-dollar RWAs? This identity search creates price uncertainty but intense developer activity beneath the surface. The Megatrend Dominating 2026: The Real-World Asset (RWA) On-Chain Rush The most powerful trend reshaping the crypto landscape in 2026 is the accelerating tokenization of everything. This isn’t about meme coins or novel consensus mechanisms; it’s about representing ownership of tangible, income-producing assets on blockchains. 1. The New Asset Classes Leading the Charge: U.S. Treasury Bonds: Platforms like Ondo Finance and traditional giants like Franklin Templeton are leading the way. Why? A tokenized T-Bill offers a global, 24/7, transparent, and high-yield “digital dollar” alternative, particularly attractive in economies with capital controls or currency instability. Private Credit and Real Estate: Tokenization is unlocking liquidity in historically illiquid markets. Fractions of commercial real estate or private loan portfolios can be traded with reduced friction and middlemen. Commodities and Carbon Credits: Gold, lithium, and even carbon offset credits are being tokenized, creating more efficient and accessible markets. 2. Why This Is a Game-Changer for “Titans”: Institutional Adoption Catalyst: Major financial institutions (Citi, JPMorgan, BlackRock) are no longer just “exploring blockchain”; they are actively launching RWA pilots. This brings trillions in traditional capital to the edge of the on-chain world. Regulatory Clarity as a Driver: Regulators in the EU (via MiCA) and the UK are providing clearer guidelines for security tokens, giving institutional players the confidence to build. The “Yield” Narrative Returns: In a world of stable BTC and ETH prices, the attractive, stable yield from tokenized T-Bills (currently 4-5%) is drawing capital into the crypto ecosystem for fundamentally new reasons. The Institutional Rebuild: Learning from the 2022-2024 Crucible The second major trend of 2026 is the professionalization and institutional rebuilding of the crypto infrastructure, forged in the fires of the previous cycle’s failures. Custody 2.0: The collapse of FTX and others led to a stark “Not Your Keys, Not Your Coins” revival, but for institutions, the solution is more nuanced. New regulated custodians offer institutional-grade security with insurance and clear regulatory status, separating asset custody from trading execution. DeFi’s Institutional Makeover: Decentralized Finance is no longer just for retail degens. Projects are building permissioned, compliance-ready liquidity pools (often for RWAs) with KYC/AML built into the smart contract layer, attracting family offices and smaller hedge funds. The Rise of the Crypto Prime Broker: A new breed of service provider is emerging, offering institutions a unified platform for custody, trading across multiple venues (both centralized and decentralized), lending, and staking—all within a compliant framework. Challenges and Risks in the 2026 Landscape This new era is not without its perils. The key risks have evolved: Regulatory Arbitrage and Fragmentation: While the EU and UK advance, the U.S. remains a patchwork of state-level actions and federal ambiguity. This creates a complex global playing field. Technological Complexity in RWA: Bridging real-world legal contracts with immutable smart contracts presents profound challenges. Who adjudicates disputes? How are off-chain events (like a tenant defaulting on rent for a tokenized property) verified on-chain? Concentration Risk: The RWA narrative, while powerful, is currently led by a handful of large, centralized traditional institutions. This risks recreating the old financial system on a new ledger, rather than creating a decentralized alternative. The “Narrative Vacuum”: With Bitcoin stable and RWA growth slow and steady, the market lacks a simple, explosive retail narrative. This can lead to periods of low liquidity and vulnerability to sudden shocks. Forward Outlook: The Path to the Next Epoch The consolidation of 2026 is setting the stage for the next major market phase. Here’s what TheGlobalTitans network is watching: The Interest Rate Catalyst: The next major directional move for Bitcoin will likely be triggered by traditional macro: central bank interest rate decisions. A pivot to cutting cycles could send a flood of capital

Value-First Memberships: The 2025 Business Pivot Beating Subscription Fatigue | TheGlobalTitans

Introduction: The Tipping Point of the Subscription Economy The promise was simple: convenience, personalization, and ongoing value for a manageable monthly fee. This propelled the subscription economy to a staggering $1.5 trillion valuation. Yet, in 2025, a silent rebellion brews in the pockets of consumers worldwide. The average user now manages 12+ recurring subscriptions, leading to widespread “subscription fatigue”—a state of passive resentment that erupts during bank statement reviews. For global business leaders, this isn’t a niche problem; it’s an existential inflection point. The old playbook of “acquire at all costs, retain with content locks” is breaking. Churn rates are creeping up, and customer acquisition costs (CAC) are becoming unsustainable. In this climate, a new breed of business titans is not just weathering the storm but architecting its successor: the Value-First Membership Model. This is not a minor tweak but a fundamental philosophical and operational pivot from extracting recurring payments to earning recurring loyalty. At TheGlobalTitans, we analyze how market leaders transform friction into fidelity. The Diagnosis: Why Pure Subscriptions Are Hitting a Wall To understand the pivot, we must diagnose the disease. The core failure of the bloated subscription model is value misalignment. Companies often mistake customer inertia for satisfaction, leading to three critical fractures: The Value-Perception Gap: When the monthly cost becomes more tangible than the service provided (the “What am I paying for?” moment), churn is inevitable. Software, media, and box services are particularly vulnerable. The Bundle Bloat Paradox: Aggressive bundling (like streaming mega-packs) initially boosts revenue but dilutes brand identity and makes individual services feel disposable. The customer feels locked in a contract, not a community. The Innovation Stalemate: With revenue seemingly “locked in,” some companies slow innovation, further widening the value gap. The service becomes a utility, vulnerable to any competitor offering a spark of novelty or respect. Global data analytics from 2024 reveal the symptoms: voluntary churn in non-essential subscriptions increased by 31% year-over-year, while the willingness to trial new subscriptions fell by nearly 20%. The market is sending a clear signal: the era of low-effort recurring revenue is over. The Prescription: Anatomy of the “Value-First” Membership Pivot The visionary response isn’t to abandon subscriptions but to evolve them into something more resilient and human-centric. The Value-First Membership is characterized by its core promise: transparency, flexibility, and tangible, evolving worth. Here’s how global titans are implementing it: 1. The Hybrid Access & Ownership ModelPioneered by companies like Adobe and now spreading to hardware and automotive, this model blends subscription access with a path to ownership or equity. For example: Software: Pay a monthly fee that accrues as credit toward a perpetual license after 24 months. Automotive: A car subscription where 40% of payments can be applied to purchase the vehicle after two years. Impact: This directly combats the “money pit” perception, aligning the company’s success with the customer’s long-term asset building. It transforms a cost into an investment. 2. The Tiered “Experiential” PyramidMoving beyond basic “Premium vs. Pro” tiers, leaders are building pyramids where each level offers a distinct experience and community tier, not just more features. Base Tier (Access): Low-cost, core functionality. Middle Tier (Community): Includes access to exclusive forums, quarterly expert webinars, and peer networking. Top Tier (Co-Creation): Offers direct influence on product roadmaps, invitation to annual flagship events, and co-branding opportunities. Case in Point: Salesforce’s Trailblazer Community and Sephora’s Beauty Insider programs excel here, making customers feel like insider partners, not passive users. 3. Dynamic, Usage-Aligned PricingStatic monthly fees are becoming archaic. The new model incorporates micro-credits, rollover benefits, and activity-based pricing. A design platform might offer a base membership with “credit packs” for premium AI renders. A fitness app may have a core subscription but allow unused live-class credits to roll over or be gifted. This creates fairness and perception of control, eliminating the guilt of underutilization that drives cancellations. 4. The “Outcomes-Over-Features” GuaranteeThis is the boldest differentiator. Companies like Zapier and HubSpot are increasingly framing their value around guaranteed outcomes—time saved, leads generated, revenue influenced—backed by data dashboards that show the ROI. This shifts the conversation from “Here’s what you get” to “Here’s what we will help you achieve.” The Global Titans Leading the Charge Let’s examine two archetypes mastering this pivot: The Agile Software Titan: Microsoft’s EvolutionMicrosoft has subtly but powerfully reshaped its Microsoft 365 subscription. Beyond software updates, it now emphasizes: Continuous Value Injection: Regular infusion of new AI-powered Copilot features across the suite, making the product demonstrably better every quarter. Value Transparency Dashboard: A tool for business admins showing license utilization, productivity metrics, and estimated ROI. Community Integration: Tight linkage with the Microsoft Learn community and certification pathways, turning a toolset into a career-advancement platform.Their pivot is from selling office software to subscribing to future-proof productivity. The Physical-Digital Hybrid: Peloton’s ReinventionAfter facing near-collapse from the post-pandemic hangover, Peloton executed a textbook pivot. It retained its hardware-software bundle but fundamentally restructured its value proposition: Flexible Tiers: Introduced a lower-cost “App Only” tier to capture a wider market, while its premium tier now includes exclusive artist series, family plan options, and member challenges with tangible rewards. Content as a Living Benefit: Instead of a static library, it frames its content as an “always-evolving studio,” with weekly live events that create appointment-based value. Community as Core Product: It doubled down on its leaderboard social features and member groups, recognizing that the accountability and camaraderie are the primary retention drivers, not the bike itself.Their lesson for all business leaders: When your physical product saturates, your membership model must become the primary product. Implementation Framework: Your 2025 Pivot Blueprint For a global business ready to initiate this pivot, TheGlobalTitans Advisory recommends this phased approach: Phase 1: The Value Audit (Weeks 1-4) Map every feature and benefit of your current offering. Conduct deep customer interviews to identify which elements they truly value versus which they ignore. Calculate your true “Value-Per-Cost” ratio from the customer’s perspective. Phase 2: The Model Redesign (Weeks 5-10) Design 2-3 hybrid tier options based on audit insights. At least one tier must include a path to equity, ownership, or a guaranteed outcome. Engineer flexibility: build in rollover capabilities, pause functions, or credit systems. Develop the metrics dashboard that will prove value delivery to the member.

Climate-Tech Titans: The Unstoppable Rise of Green Unicorns Shaping Global Markets | TheGlobalTitans

Introduction: The New Titans of Industry In boardrooms from Silicon Valley to Singapore, a seismic shift is occurring. While tech giants once dominated unicorn status with software and platforms, a new breed of visionary companies is emerging—those tackling humanity’s greatest challenge: climate change. These climate-tech titans are not just building businesses; they’re architecting the foundation of our sustainable future while delivering staggering returns to early investors. At TheGlobalTitans, we track how these innovators transform from ambitious startups into global powerhouses reshaping entire industries. Across global markets, venture capital is flowing into climate solutions at unprecedented rates, with over $70 billion invested in 2024 alone. This isn’t merely a trend; it’s the great capital reallocation of our century—where funds once funneled into fossil fuels now accelerate decarbonization technologies. For business leaders, entrepreneurs, and investors monitoring the stock market’s evolution, understanding this landscape is no longer optional—it’s essential for future-proofing portfolios and strategic planning. The Current Landscape: Where Climate and Capital Converge The climate-tech sector has matured dramatically since its early days of solar panels and wind turbines. Today’s climate unicorns—private companies valued over $1 billion—operate across diverse domains: Carbon Capture and Utilization (CCU): Companies like Climeworks (Switzerland) and CarbonCure (Canada) are turning emissions into valuable products, from building materials to synthetic fuels. Green Hydrogen Production: With governments worldwide committing billions to hydrogen economies, startups like Electric Hydrogen (US) and Hysata (Australia) are scaling production of the zero-carbon fuel. Alternative Protein and Sustainable Agriculture: Beyond Meat’s public market journey paved the way for next-generation food tech companies like Upside Foods and Impossible Foods, now valued in the multi-billions. Grid-Scale Energy Storage: As renewable penetration grows, companies like Form Energy (developing iron-air batteries) and ESS Inc. (flow batteries) solve the intermittency challenge. Climate Risk Analytics: In an era of increasing weather volatility, platforms like ClimateAI and Jupiter Intelligence provide critical forecasting for businesses and governments. What’s particularly notable in 2025 is the geographical diversification of climate innovation. While Silicon Valley remains important, significant hubs have emerged in the European Union (especially Germany and Scandinavia), Southeast Asia (Singapore as a clean tech gateway), and Australia (a renewable energy testing ground). TheGlobalTitans network spans these regions, connecting visionaries who recognize that climate solutions must be globally applicable yet locally adaptable. Market Implications: How Climate Tech Moves Markets The rise of climate unicorns isn’t occurring in a vacuum—it’s creating ripple effects across traditional financial markets: Stock Market Sector Rotation: Energy sector composition is transforming. The S&P Global Clean Energy Index has outperformed traditional energy indices for three consecutive years, signaling investor preference shift. Traditional oil giants like Shell and BP now allocate 25-30% of capital expenditure to renewables and decarbonization projects—partly through partnerships with or acquisitions of climate-tech startups. Regulatory Catalysts: The European Union’s Carbon Border Adjustment Mechanism (CBAM), now fully implemented, creates a tangible price advantage for low-carbon products. Similarly, the US Inflation Reduction Act continues to catalyze investments through substantial tax credits for clean energy deployment and manufacturing. Savvy investors monitor which startups are best positioned to benefit from these policy tailwinds. Valuation Premiums: Public market investors now assign “green premiums” to companies with credible decarbonization pathways. Analysis by TheGlobalTitans Research indicates that companies in carbon-intensive sectors with science-based transition plans trade at 15-20% higher valuation multiples than laggards. This creates acquisition opportunities for climate-tech companies whose solutions help established corporations bridge their emissions gaps. ESG Integration Evolution: Environmental, Social, and Governance (ESG) investing has matured from exclusionary screening to active engagement and transition financing. The climate-tech unicorns providing measurable decarbonization solutions are becoming essential partners for ESG-focused funds seeking both impact and returns. Investment Strategies for the Climate-Tech Era For investors seeking to participate in this transformation, several approaches have emerged: 1. Venture Capital Allocation: Specialist climate-tech VC funds now offer diversified exposure across technologies and development stages. Top-performing funds like Lowercarbon Capital and Breakthrough Energy Ventures focus on the “hard tech” solutions with potential for gigaton-scale impact. 2. Public Market Opportunities: While most climate unicorns remain private, the IPO pipeline is robust. Investors can gain exposure through: SPAC Mergers: Several climate-tech companies have gone public via SPACs, though post-2022, due diligence has intensified. ETFs and Mutual Funds: Thematic funds like iShares Global Clean Energy ETF (ICLN) and Invesco Solar ETF (TAN) provide diversified exposure. Corporate Venture Arms: Established companies like Microsoft’s Climate Innovation Fund directly invest in and partner with climate startups, creating indirect exposure through equity holdings. 3. Geographic Considerations: Different regions offer specialized opportunities: North America: Strong in carbon tech, advanced renewables, and sustainable agriculture Europe: Leadership in green hydrogen, circular economy solutions, and climate software Asia-Pacific: Dominance in battery technology, solar manufacturing, and EV supply chains 4. Stage Diversification: A balanced portfolio might include: Early-stage (pre-seed/Series A): Higher risk but potential for outsized returns Growth-stage (Series B/C): More proven technologies scaling toward commercialization Pre-IPO/late-stage: Reduced risk profile with clearer path to liquidity events TheGlobalTitans advisory team consistently emphasizes that successful climate investing requires both technological and policy literacy. Understanding which technologies have crossed the “commercialization valley of death” and which policies create favorable economics separates trend followers from strategic investors. Challenges and Risks: Navigating the Green Frontier Despite the optimism, climate-tech investing faces distinct challenges: Technology Risk: Many solutions are still at pilot or demonstration scale. Hydrogen electrolyzers, direct air capture, and long-duration storage require further efficiency improvements and cost reductions to reach widespread adoption. Policy Dependency: The sector remains sensitive to political shifts. While climate policy has shown remarkable bipartisan support in many markets, regulatory stability cannot be taken for granted. Greenwashing Concerns: As capital floods the sector, distinguishing genuinely transformative technologies from incremental improvements marketed as breakthroughs becomes crucial. TheGlobalTitans due diligence framework emphasizes measurable emissions impact and scalability assessments when evaluating opportunities. Capital Intensity and Long Timelines: Unlike software startups, many climate solutions require significant infrastructure and face longer paths to profitability. Investors must align their expectations with these physical and temporal realities. Supply Chain Constraints: Critical minerals for batteries, rare earth elements for wind turbines, and specialized components for carbon capture systems face potential bottlenecks as demand accelerates globally.

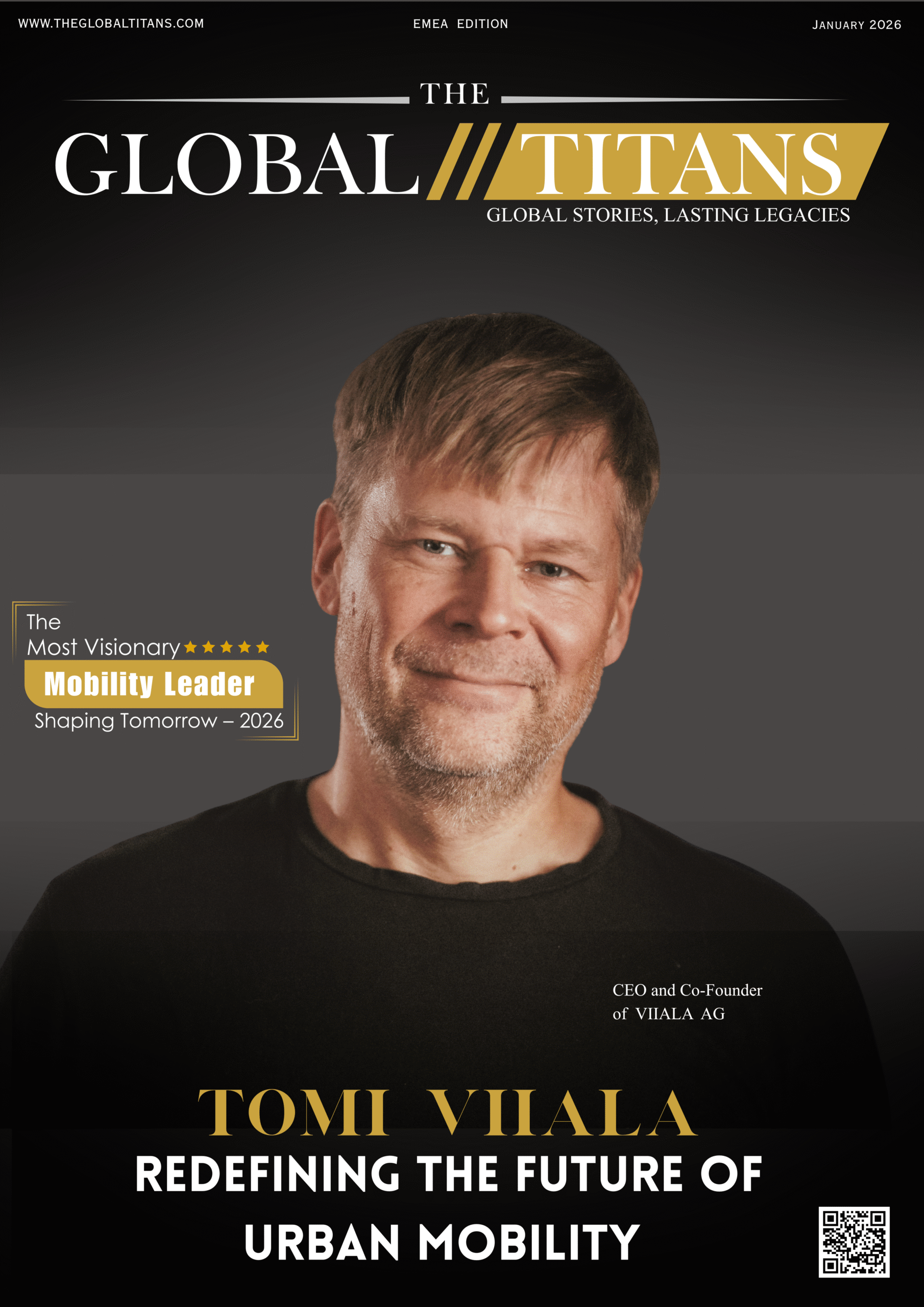

The Most Visionary Mobility Leader Shaping Tomorrow – 2026

One of the Most Visionary Leader Reinventing Financial Services – 2026

Explore the Digital Magazine In this edition of The Global Titans, we feature Stanley Moskowitz — a leader redefining finance through empathy and purpose.With over four decades of experience, he has consistently placed people and trust above transactions.From leading Petroleum & Franchise Capital to shaping Feeasy, his work focuses on simplifying finance and empowering individuals.Stanley Moskowitz’s legacy shows that purpose-driven finance can truly change lives. Read More

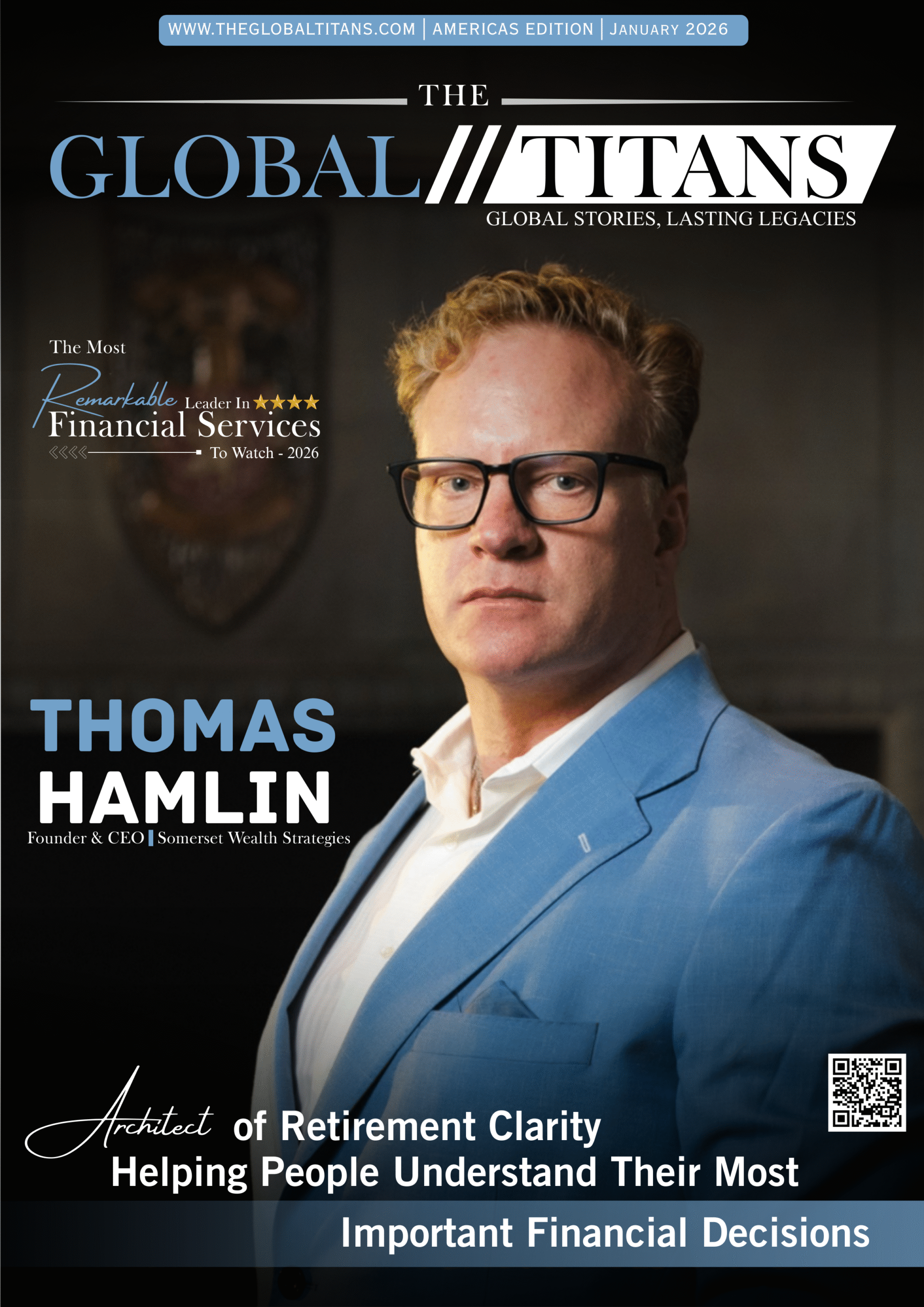

The Most Remarkable Leader in Financial Services to Watch – 2026

Explore the Digital Magazine In this edition of The Global Titans, we spotlight Thomas Hamlin — a founder redefining wealth management through trust and structure.As Founder & CEO of the Somerset Family of Companies, he builds institutions designed for durability, not headlines.His leadership prioritizes long-term confidence, client transparency, and operational discipline.By integrating technology to strengthen judgment, he balances innovation with stability.Thomas Hamlin’s legacy reflects that true financial leadership is built on integrity, resilience, and generational vision. Read More

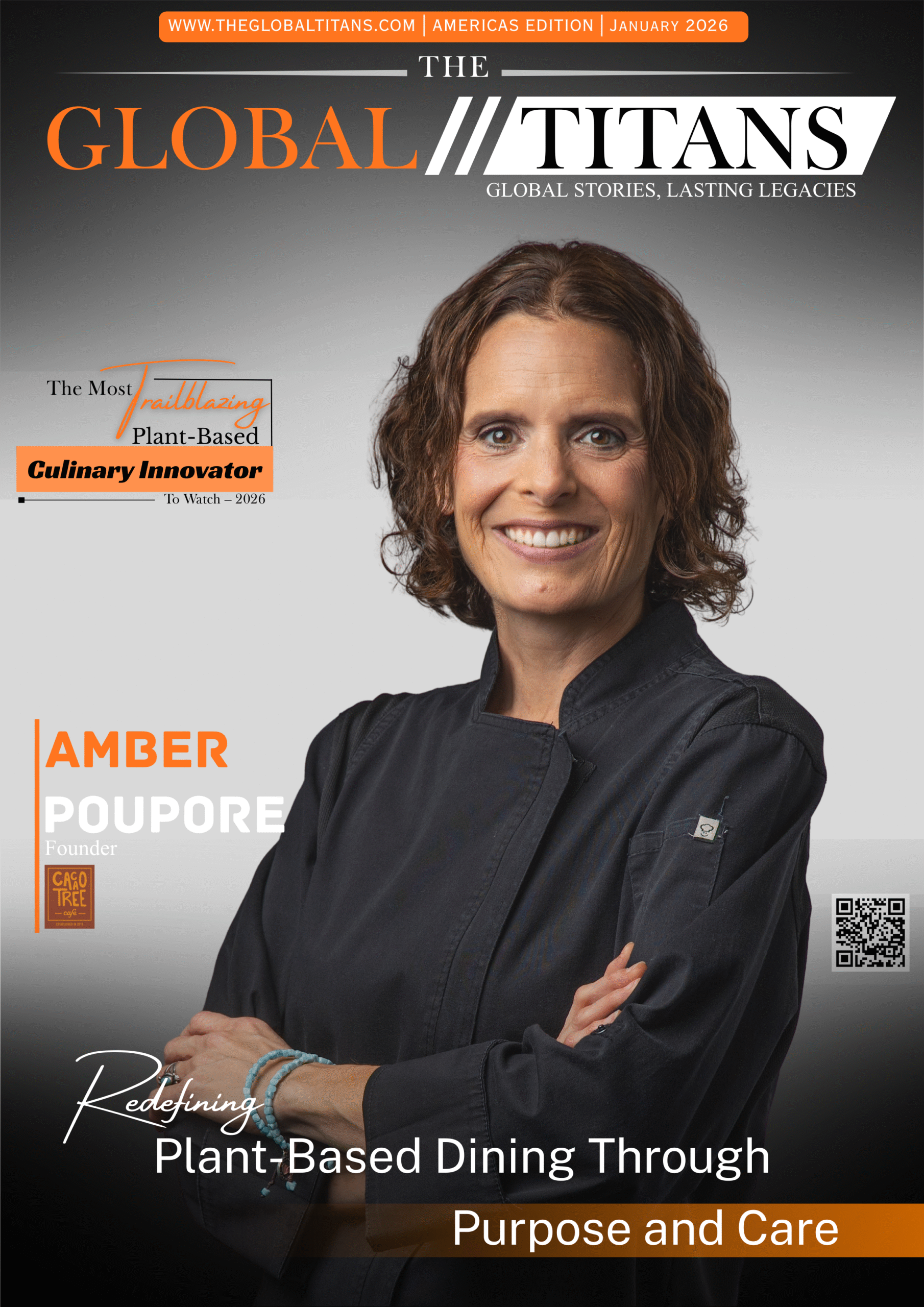

The Most Trailblazing Plant-Based Culinary Innovator To Watch – 2026

Explore the Digital Magazine In this edition of The Global Titans, we feature Amber Poupore — a leader shaping plant-based dining through discipline and long-term vision.As Founder and Chief Operator of Cacao Tree Cafe, she proves that conscious food brands can scale with structure and integrity.With decades of hands-on experience, Amber leads with operational clarity, ingredient integrity, and guest trust.Her work embeds sustainability, team development, and nourishment into daily business systems.Amber Poupore’s leadership shows that businesses built with intention are designed to last. Read More